By TheLowInterest 21 May, 2026

By The Low Interest / EMI Calculator / May 2026

Managing a personal loan shouldn't feel like a guessing game. Many borrowers make the mistake of focusing strictly on the total loan amount or the advertised interest rate, but it is the Equated Monthly Instalment (EMI) that directly impacts your day-to-day finances.

If your monthly repayment amount is too high, it can quietly strain your budget and impact your savings. Utilizing an online personal loan EMI calculator is the smartest way to map out your repayment schedule, experiment with different tenures, and protect your financial health.

This guide breaks down everything you need to know about how to calculate loan EMI India, evaluating the true cost of borrowing, and strategic loan repayment planning to ensure you stay financially comfortable.

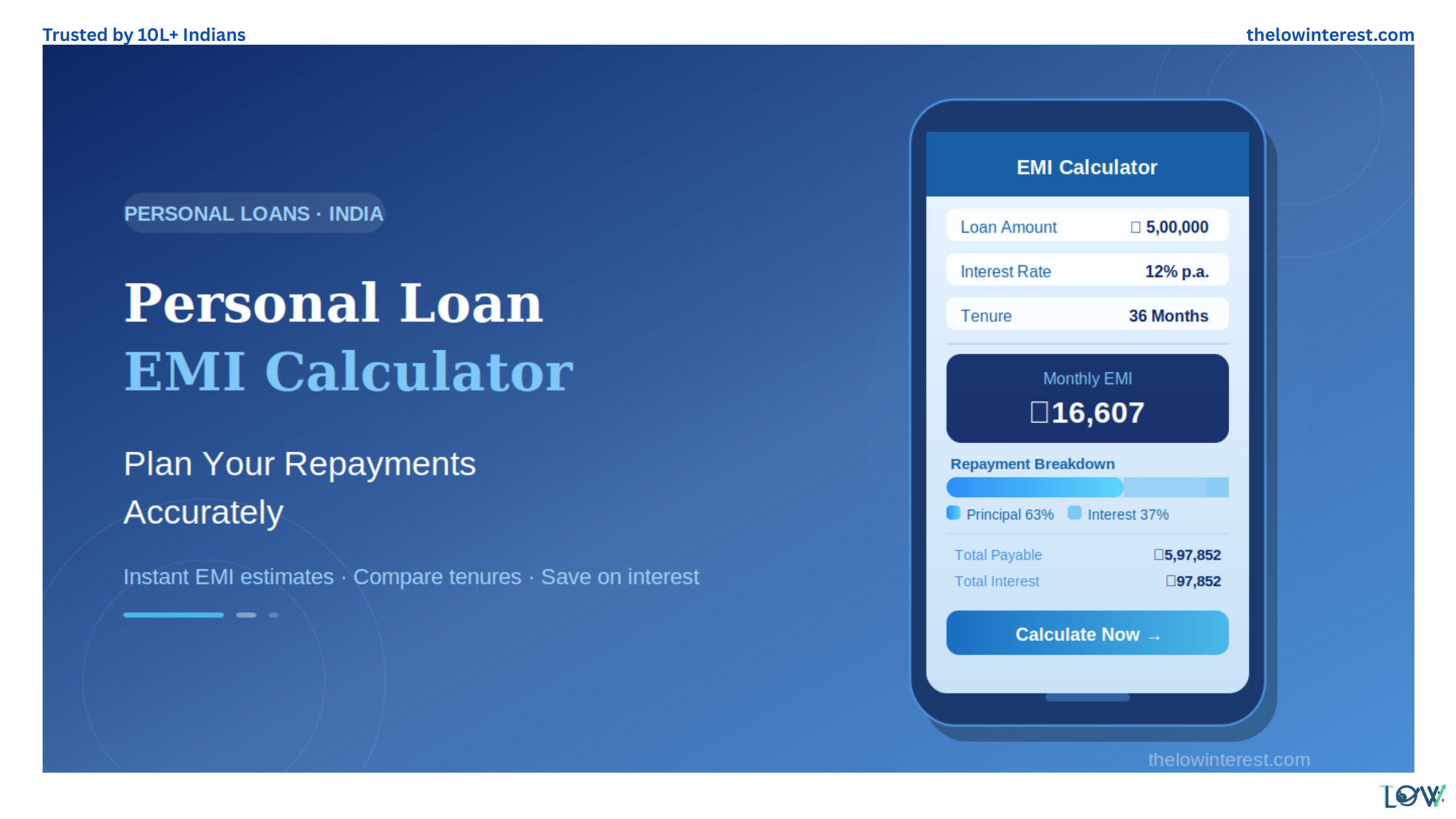

A personal loan EMI is a fixed amount paid to a bank or Non-Banking Financial Company (NBFC) on a specific date each month until the loan is fully paid off.

Every single payment you make is split into two parts:

Principal Repayment: The actual portion of the initial money you borrowed.

Interest Charges: The cost of borrowing that money, calculated by the lender.

For fixed-rate personal loans, this monthly obligation remains exactly the same throughout your entire personal loan tenure, making it highly predictable for budgeting.

Lenders across India compute your monthly payment using a standard mathematical formula:

EMI=(1+R)N−1P×R×(1+R)N

Where:

P = Principal loan amount

R = Monthly interest rate (Annual rate divided by 12 divided by 100)

N = Total loan repayment period in months

While doing this math manually can be tedious, an online personal loan EMI calculator does the work instantly. You only need to plug in three key figures: the total money required, the interest rate offered, and the desired repayment timeframe. The system will immediately display your monthly payment, the total interest payable, and the absolute final amount you will hand back to the lender.

Note: These figures are illustrative approximations. Actual amounts may vary slightly based on processing fees, specific lender calculations, and your individual credit profile.

Choosing the right repayment period is a direct trade-off between monthly cash flow and long-term interest costs.

Short Repayment Tenure: Leads to higher monthly payments but clears the debt quickly and saves a significant amount on overall interest.

Long Repayment Tenure: Brings down the immediate monthly payment burden, making it easier on your wallet today, but causes the total interest costs to balloon over time.

For example, looking at the table above for a ₹5 Lakh loan at a 12% interest rate, extending your repayment window from 3 years to 5 years drops your monthly payment by roughly ₹5,485. However, that choice will cost you an extra ₹69,468 in pure interest charges by the end of the loan.

The Principal Sum: Borrowing more money naturally results in higher monthly payments and a larger overall debt burden. Only borrow exactly what you need.

The Offered Interest Rate: Lower rates decrease both the monthly obligation and the long-term cost of the debt.

Your Credit Score: A high credit score signals low risk to financial institutions, allows you to secure the most competitive interest rate in market.

Income Stability: Lenders verify your employment history and steady cash inflow to evaluate your true repayment capacity before approving applications.

Looking Only at the Monthly Payment: A low monthly payment might seem highly attractive, but if it spans an excessively long timeframe, you could end up paying double the original loan amount in interest.

Skipping the Comparison Phase: Interest rates, processing fees, and foreclosure terms vary drastically between traditional banks and modern digital lenders. Always weigh multiple offers.

Maxing Out Your Debt Capacity: Financial planners generally advise keeping your total monthly debt obligations—including home, car, and personal loans—well under 40% of your net monthly take-home salary.

If you want to secure the lowest possible interest rate and minimize your financial liabilities, focus on these actionable steps:

Optimize Your Credit Profile: Pay off existing credit card balances and ensure zero delayed payments for at least six months before applying to boost your score.

Negotiate Terms Explicitly: If you have an established, long-term relationship with your bank, use your clean track record to request a waiver on processing fees or a reduction in the interest rate.

Plan Regular Part-Prepayments: Whenever you receive a workplace bonus or a financial windfall, use those funds to pay down the loan principal early. This directly reduces the remaining tenure or lowers your ongoing monthly payments.

When you are ready to move forward with an online application, ensuring you have the correct documentation in place will accelerate the processing time.

Identity & Address Verification (PAN Card, valid government-issued address proofs)

Income Verification (Recent salary slips, Form 16, or Income Tax Returns)

Financial Statements (Updated bank account statements for the last 3 to 6 months)

Use an online calculator to identify your ideal loan structure.

Compare financial institutions to locate competitive interest rates.

Complete the online digital application form securely.

Submit your structural verification and income documents for verification.

Review the loan agreement carefully before accepting final disbursal.

A personal loan is a highly effective financial tool for managing unexpected emergencies or funding milestone life events. However, the secret to a stress-free borrowing experience lies entirely in comprehensive loan repayment planning.

By evaluating your options with a personal loan EMI calculator before making a formal commitment, you can enter into a credit agreement with full transparency, knowing exactly how much you will owe every month and ensuring your personal budget remains perfectly balanced.

.png)

.png)